Getting Ready for Insurance

Obtaining the right coverage requires a strong portfolio and robust hiring practices

Este es nuestro intento de convertir las historias en audio español usando Inteligencia Artificial. Aún así le recomendamos que reconfirme ciertas palabras clave y temas. ArborTIMES no garantiza ni se responsabiliza de la conversión del inglés al español de los relatos.

Insurance in the tree care industry can be a moving target, with costs linked to industry trends and practices. Here’s why it’s important to put your best foot forward when shopping around.

Insurance is a highly detailed and expensive industry that can leave many tree care business owners scratching their heads about how to best protect their business and employees.

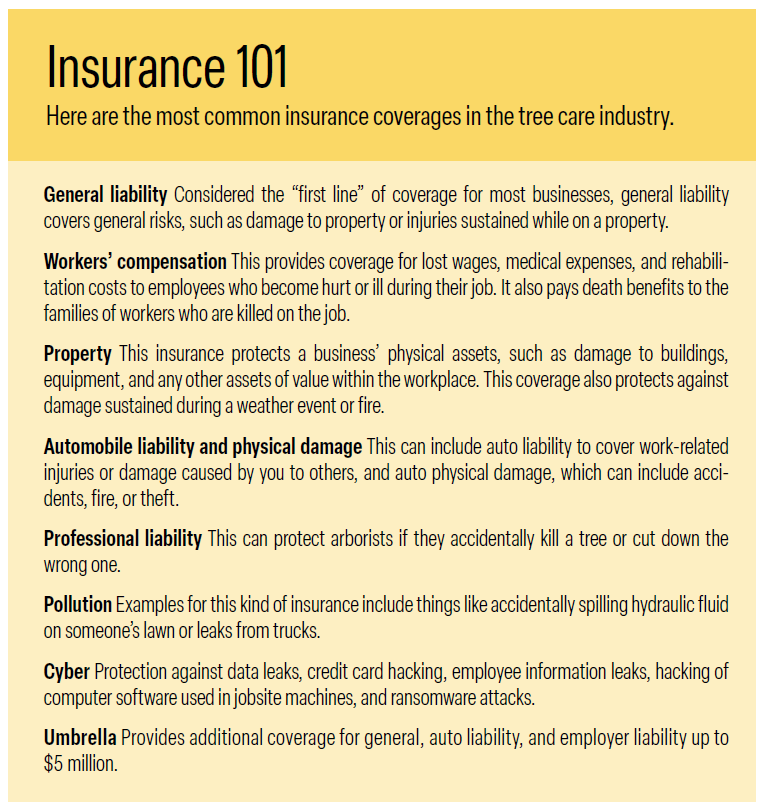

Because tree care work involves heavy machinery and technical work, it requires specialized insurance to cover a range of situations. These can include job site accidents, personal injury, vehicle and machine accidents, cyber attacks, pollution, professional liability, and more.

“The stakes are higher because it’s with more massive equipment,” says Thomas Doherty, senior vice president of specialty programs at NIP Group, which provides insurance, underwriting, and risk management services for tree care companies.

When shopping for insurance, it can be hard to imagine and prepare for the right worst-case scenario. With insurance costs related to risk, tree care insurance can be expensive. What’s more, these costs can fluctuate according to trends and safety practices within the tree care industry.

Ultimately, the best way to keep insurance costs down is for business owners to show they prioritize workplace safety.

No one likes to wade through confusing insurance policies, nor does anyone want to choose a policy only to worry whether it truly meets their needs. Navigating insurance intricacies and learning to speak the language is an important first step to keep your employees and business safe.

“Tree care is a volatile business. It’s one of the businesses where — and it does happen weekly — where someone could lose their life performing the task,” says Mark Shipp, practice leader for Hub Arbor Insurance Group. “Really, what you must understand is what is the true appetite for your business? Do [insurance providers] really understand what you are doing?”

Why Insurance Matters

It bears repeating that tree care work is among the most dangerous kind there is in the U.S. While construction had the most workplace deaths in 2021, the agriculture, forestry, fishing, and hunting industry (which includes tree care work) experienced the highest death rate, according to the National Safety Council.

When injuries and fatalities do occur, a lack of safety equipment is usually to blame.

A five-year study in the heavily forested area of Westchester, NY, for example, sought to understand why a local trauma center was seeing an “alarming” number of tree-related brain and spinal injuries.

The study found “that serious injuries, many of which required neurosurgical intervention, occurred from working in a heavily forested area without proper safety protection” (PPE.)

Even with PPE, injuries can still occur. This is why workers’ compensation insurance is mandated for business in nearly every state, except Texas.

“Workers’ comp can be waived in most states with a specific filing if you are an owner and have no employees,” says Brian Fain, a commercial insurance advisor with Ferguson & McGuire. “If you have one or more employees, you are required by the majority of states to carry workers’ compensation.”

Workers’ comp isn’t the only insurance worry among business owners. Litigated claims in the tree care industry increased from 2.1% in February 2021 to 7.1% in 2022, according to a report by NIP Group.

Professional liability is another insurance that’s usually recommended for tree care companies. This covers situations where arborists cut down the wrong tree or threaten the health of trees.

“If you use the wrong chemical you could kill the tree,” Doherty says.

Having professional liability coverage is just one way insurance can improve a tree care business’ credibility with customers.

Any consumer can ask for a general liability certificate, reminds Doherty, and this is especially important when people are working along tight property lines, where injury to people or assets is possible.

With liability lurking around every corner, it’s becoming even more important to keep up with — and even stay ahead of — industry trends.

Rising Insurance Costs

According to Doherty, workers’ compensation costs have gone down over the years, with new technology helping to make the industry safer for employees.

What has increased, however, is automobile insurance and third-party bodily injury claims, accidents that can occur to people unrelated to the tree care work, such as children playing in a park next to a job site.

Auto accidents are among the leading causes of fatalities for tree care professionals, often due to overloading, improper driving techniques, and failure to conduct proper maintenance, according to NIP Group’s report.

First-party auto losses per 1,000 vehicles increased by 80% at the end of 2021, compared to the same time in 2020, according to the report. Additionally, closed files on auto physical damage losses were 16% higher at the final quarter of February 2022 than the previous nine months combined.

A surge in catalytic converter thefts hasn’t helped either. Thefts jumped dramatically from just 1,298 in 2018 to 14,433 in 2020, according to a report by the National Insurance Crime Bureau.

Attract the Best Rates

As tree care companies look for insurance providers, the advice is clear: be prepared to show you are low risk.

“The tree company should know their own score,” says Shipp.

This score is a company’s loss ratio, which represents the amount of premiums paid in by a business versus claims paid out by the insurance company. Having this type of historical credibility, Shipp says, can show an insurance company that a business knows how to reduce the potential for claims.

Presenting a solid portfolio is the best way to show an insurance company that your company is worth insuring. Blackman suggests preparing portfolios that include five years of loss runs and ACORD certificates to clearly communicate insurance coverage for each line of business.

A supplemental questionnaire might also be required to answer questions regarding the tree care company’s safety program, vehicle maintenance, driver training and formal safety training, Blackman adds.

Good accounting and bookkeeping become paramount in tracking these metrics. These can also be used to show insurance companies that companies can make premium payments on time and not have any lapses in coverage.

“[This can be] just as bad as having bad claims,” says Shipp.

Another way for a business to prove its worth is to implement technology and other solutions meant to offset high-level risks from one of the costliest components of tree work: auto accidents.

These can include using GPS trackers or dashboard cams in work vehicles, such as those offered by Samsara, which specializes in fleet management.

With one eye on the driver and another on the road in front, dashboard cams may be a worthy investment to help defend companies from ”nuclear” and “thermonuclear” verdicts up to $10 million.

Hiring practices is another area that has become tightly interwoven with insurance. Often, a rigorous hiring process can help keep costs down.

“Having a driver screening process is tantamount to risk reduction,” says Shipp.

This can include checking references, drug testing, conducting a background check, and reviewing driving records. It is not uncommon for insurance companies servicing the tree care industry to turn down companies if a faulty driver may provide an exceptionally high risk.

Doherty also suggests hiring more experienced drivers, preferably over the age of 25.

When applying for insurance, be prepared for a lot of dialogue with the policy underwriter. They will want to know about safety protocols, ongoing training, certification, and accreditation.

“If an underwriter has no idea what you are doing for training, why would they consider favorable rates or even offer a company a quote?” Fain asks.

Finding the Right Carrier

Insurance in the tree care industry needs to be carefully examined for cost, coverage, and relevancy. Coverage should be specific to the tree care industry and not just landscape work, which uses lighter equipment and presents fewer risks.

“There are many carriers that will write tree care operations, but they don’t all provide the same coverage,” says Jeff Blackman, program manager at ArborMAX. “The insurance customer can’t make an informed choice just by looking at the premium alone. Limits and industry-specific coverages need to be considered as well.”

Blackman suggests asking about arborist professional liability and coverage for chemical applications, as these are good indicators of industry-specific needs. Failure to cover heavy equipment could be a cautionary flag as well, he adds.

“The right agent will be one that has an understanding of the tree care industry, is willing to spend time with the client to get a clear picture of their operation, and submit it to the correct carriers,” Blackman says.

Cheaper is not always better when it comes to insurance. A tree care company needs to weigh out bottom-line costs with the coverages they include, as not all are created equal.

“You may find cheaper options, but it is important to stick with carriers that have provided coverage to the tree care industry for years,” Blackman says. “They won’t always be the least expensive, but they will be staffed by people that understand the work you do.”

Conclusion

Tree care work presents a precarious business, and insurance is vital to ensure the safety of workers and others impacted by their work. Navigating insurance can be highly nuanced and it can be difficult to understand how much coverage is needed.

When negotiating a policy, make sure your bookkeeping is organized and can provide easy answers to insurance underwriters. Try to integrate new technologies and solutions when possible, and commit to hiring and training safe drivers and workers.

At the same time, tree care companies should screen prospective insurance companies by asking questions and ensure they are familiar with insurance terms. Being precise with language is key to getting what you need.

Ultimately, taking the time to build a strong relationship with your insurance provider will help ensure the safety of your workers and your business.